|

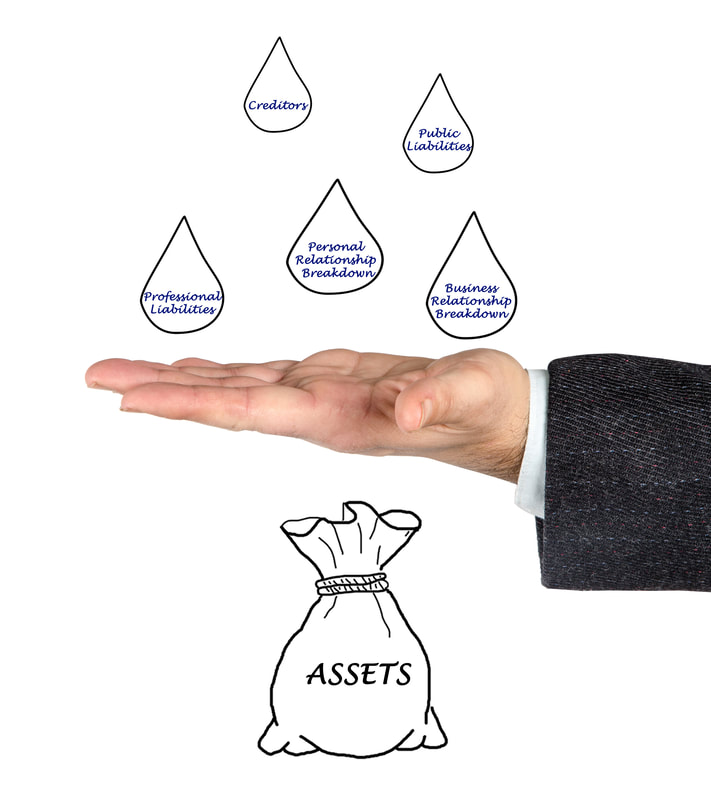

Asset protection is the adoption of advance planning techniques that place one's assets beyond the reach of creditors. It does not involve fraudulent or illegal activity. It is based upon proven sophisticated combinations of business and estate planning techniques. The methods employed include the use of financial products and legal structures domestically and offshore.

There are two general objectives behind asset protection strategies. One is to place assets beyond the reach of creditors, through the creation of legal structures or relationships. Another is to position those assets to deter creditors from pursuing those assets or to hinder their ability to successfully pursue them. Except in extremely limited and well-defined circumstances (e.g. bankruptcy or federally backed loans) there are no penalties, either civil or criminal, for engaging in asset protection. It is important to implement a asset protection plan before any claims arise. Think of it like getting a flu shot. If you get a flu shot before flu season then you will most likely not be affected by the flu but the more into flu season you wait, the more likely you are to contract and fall ill to the flu. At Private Client Advisers we focus on creating the right Asset Protection Plan for you based on you financially specific and ever-changing needs. |

|

|

|

|